The Digital Markets Act unlocks new payment options for app developers and lets them start saving money using third-party solutions. In the article, we explore the impact this law has on mobile payments, take a closer look at alternative payment solutions, and provide you with an overview of fees you'll have to pay. See how you can save money!

The Digital Markets Act (DMA) is a landmark European law which entered into force fully and definitely just last month. The aim of this document is to rein in the dominance of the biggest tech hegemons— the so-called “gatekeepers”—and make access to both their platforms and users easier and simpler.

What’s in it for you? Well, the reforms brought about by this legislation will finally allow businesses—the developers and owners of apps—to select an alternative payment service provider instead of the one originally offered by the platform. This will be possible in areas such as Google’s, or Apple’s, in-app payments infrastructure. The ultimate result? You’ll have ample opportunity to choose the payment solution most suitable to your needs, as well as to reduce costs. Consequently, you will deliver better end-user experiences.

In this article, we’ll remind you what DMA is, explain what implications it will have for app owners and developers, as well as end users, and how it will affect payments and payment processor options. We’ll explore the key provisions of this law related to payment services, the DMA’s impact on organizations, businesses and users in the digital space, the regulation’s value and support for everyone in the digital realm.

Read on to get up to speed on one of the hottest topics in the business world of mobile application development and the payments’ infrastructure industry right now.

Introduction

The DMA has been on the statute book since November 2022. However, it is only from March 6 of this year that those companies that were named gatekeepers must follow the rules set for them by the EU. This piece of legislation has admittedly been put in place so that the internet ‘becomes a fairer place’ by finally ‘bridling’ the Big Five—Alphabet (Google), Amazon, Apple, Meta, and Microsoft. It is no secret that the Big Five’s dominance in their respective markets, as well as lack of any meaningful regulation, have been quite problematic. So, leveling the enormous control they enjoy over the industry has long been overdue.

Six companies have been chosen as ‘gatekeepers’ in September 2023: Alphabet (Google and YouTube), Amazon, Apple, ByteDance (TikTok), Meta (Facebook, Instagram and WhatsApp), and Microsoft (LinkedIn and Windows). It goes without saying that these companies specifically have been enjoying excessive influence on the way we access the internet. These companies were identified as gatekeepers after they met the European Commission’s criteria. For now, there are only six such companies, but there is room for future gatekeepers to emerge in the future.

Giving developers and app owners more control over payment options is just one of many components of DMA. The overall hope is that it will increase fairness and boost competition on digital platforms, as Google and Apple will now have to accept payments through third-party payment solutions. And DMA itself is just part of the wider EU Digital Strategy process.

Both Google Play and App Store have been enjoying their market hegemony for more than a decade, during which time they remained largely unchallenged. This is set to change. DMA is coming like a storm, significantly impacting the business of mobile monetization. From now on, developers will have more options on how to make revenue and handle the money aspect than ever.

If you want to learn more about DMA, its purpose, and how it positively impacts mobile apps, its developers, and its millions of users, then check out our previous article in this series – Your Go-To Guide To Digital Market’s Act.

Before delving deeper into how DMA is impacting payments or how Google and Apple are complying with the law, let’s first find out what it was like before. Read on.

How Mobile Payments Worked Before Digital Markets Act

For quite some time prior to the launch of DMA, payment options on Google and Apple devices were tightly controlled. Both Google and Apple required their payment systems to be used as the main ones, and sometimes as the only ones, when the services provided by app owners were fully digital. Think Spotify, Tinder or Minecraft.

This means that in cases where we offered customers some physical services in the application (e.g., a hairdresser) or goods (we ran a store, e.g., Allegro), we could use alternative payment providers. There were some exceptions in a single market and the Asian market where other payments could be used alongside Google payments.

Under the old system, the only way to install apps on a device was to use the App Store (owned by Apple) in the case of iPhones or the Play Store, in the case of Android phones. And in-app payments had to go through Apple Pay and Google Pay; users could not pay directly with credit cards or use a QR code to navigate off-platform, for instance.

How DMA impacts payments

The DMA’s Article 5 introduces significant changes from a payment processor sector perspective. It states that the gatekeeper’s platforms may no longer require app developers to stick to their own payment processors or systems. They will now have to accept payments made using a third-party payment processor. This promises the long-awaited unbundling of payment services from gatekeepers’ core platform services. Which will result in improved competition and better choice for online businesses in terms of their payment options.

This shift will allow businesses and app developers more flexibility and freedom in choosing their payment service providers, enabling them to base their decisions on factors such as their business model, customers’ preferences, costs, and settlement times. By breaking down the monopolistic control gatekeepers had over payment services, the DMA empowers developers with and enables businesses to have greater flexibility in managing their payment ecosystems.

Why consider using alternative payment systems

Cost Comparison

Google Play Store is charging at least a 15% fee per transaction. However, app developers should expect a 30% fee for earnings in excess of $1M (USD) revenue earned by the developer each year. Any transaction that Apple processes for you will be subject to the 30% transaction fee as well. The exact numbers and specific cases will be discussed further in the article.

Transaction fees, which are this high, are one of the many reasons that spurred the EU commission to create and develop the DMA in the first place. And these fees are the main reason why app developers would be wise to consider using an alternative payment system.

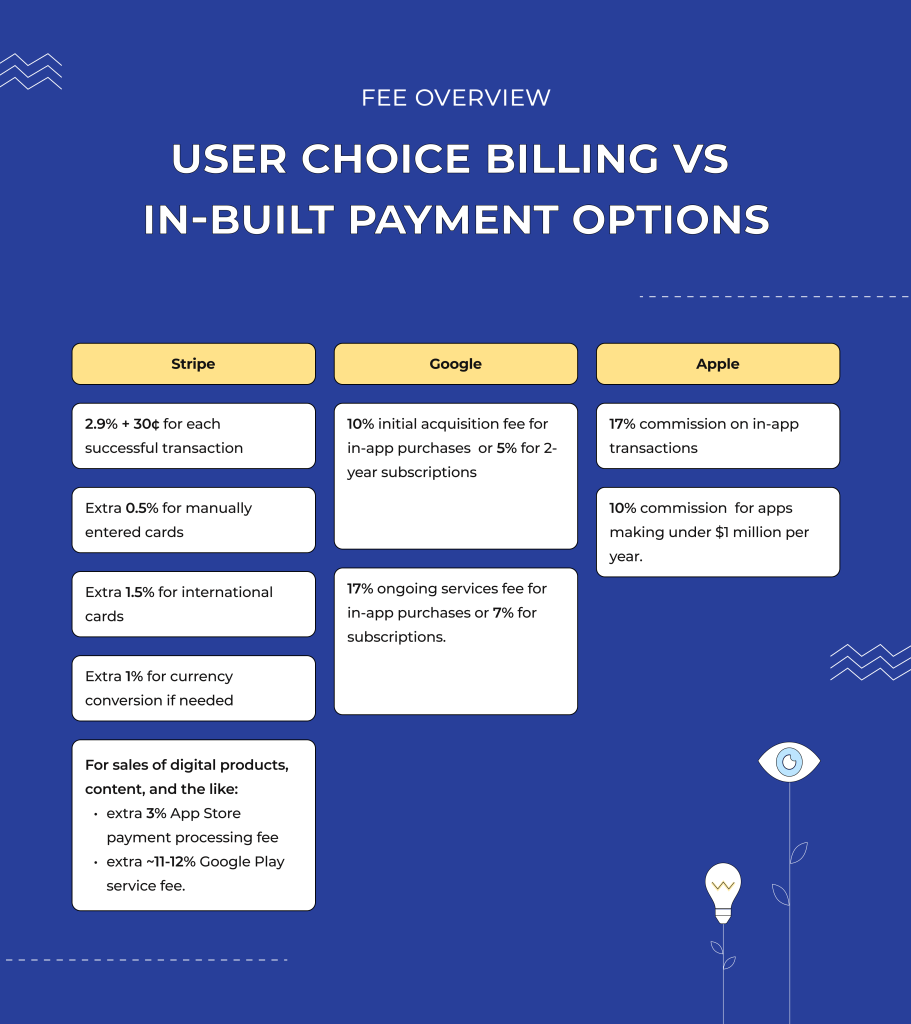

For example, when using an alternative payment solution such as Stripe, there will also be transaction fees, but much smaller. Stripe charges 2.9% + 30¢ for each successful transaction. Additional fees apply for specific scenarios: 0.5% for manually entered cards, 1.5% for international cards, and 1% if currency conversion is necessary.

Invoicing Issues

In B2B solutions, there are issues with getting a proper invoice from Apple or Google. To get an invoice for purchasing an app, businesses would need to have a developer’s account, which costs $200. Another way to get an invoice is by asking tech support for it ‘manually’. Apple support provides such an opportunity, whereas Google is less clear on this matter.

With an alternative payment solution provider, you will no longer have to worry about getting invoices. Alternative payment providers, such as Stripe, will provide you with an itemized list of goods and services rendered — including the cost, quantity, and any applicable taxes — while also collecting payment through a range of supported Payment Methods, apart from Stripe’s own in-built payment method. It allows you to manage your invoices through the API or Dashboard, and customize how they look through your Invoice template settings. Sounds like a day and night change from Google and Apple invoicing approach, right?

How Google complies with the DMA

Payments-related changes

In response to DMA, Google announced the introduction of two new fees that will apply to its External Offers program. Under this program, Play Store developers will be able to lead their users in the EEA outside their app. This approach is similar to the one taken by Apple. Apple reduced its App Store commissions in the EU yet added a new fee—the Core Technology Fee in its case—too.

The two fees that will accompany External Offers program transactions from now on are:

An initial acquisition fee: 10% for in-app purchases or 5% for subscriptions for two years.

An ongoing services fee: 17% for in-app purchases or 7% for subscriptions.

It’s important to note that developers can opt out of these fees, if the user agrees, after two years. Obtaining user consent is vital because, during the installation of the app, users signed up for services like parental controls, security scanning, fraud prevention and continuous app updates. Developers will also be tasked with reporting transactions involving those users who opt to continue to receive Play Store services.

Google also provided some more additional information:

this program is opt-out only;

it applies to games and apps alike;

developers who have several apps on the store can opt-in only some of their apps.

developers would have to register for the program as a business, not as an individual

developers can simultaneously use both Google Play’s billing system and participate in the external offers program.

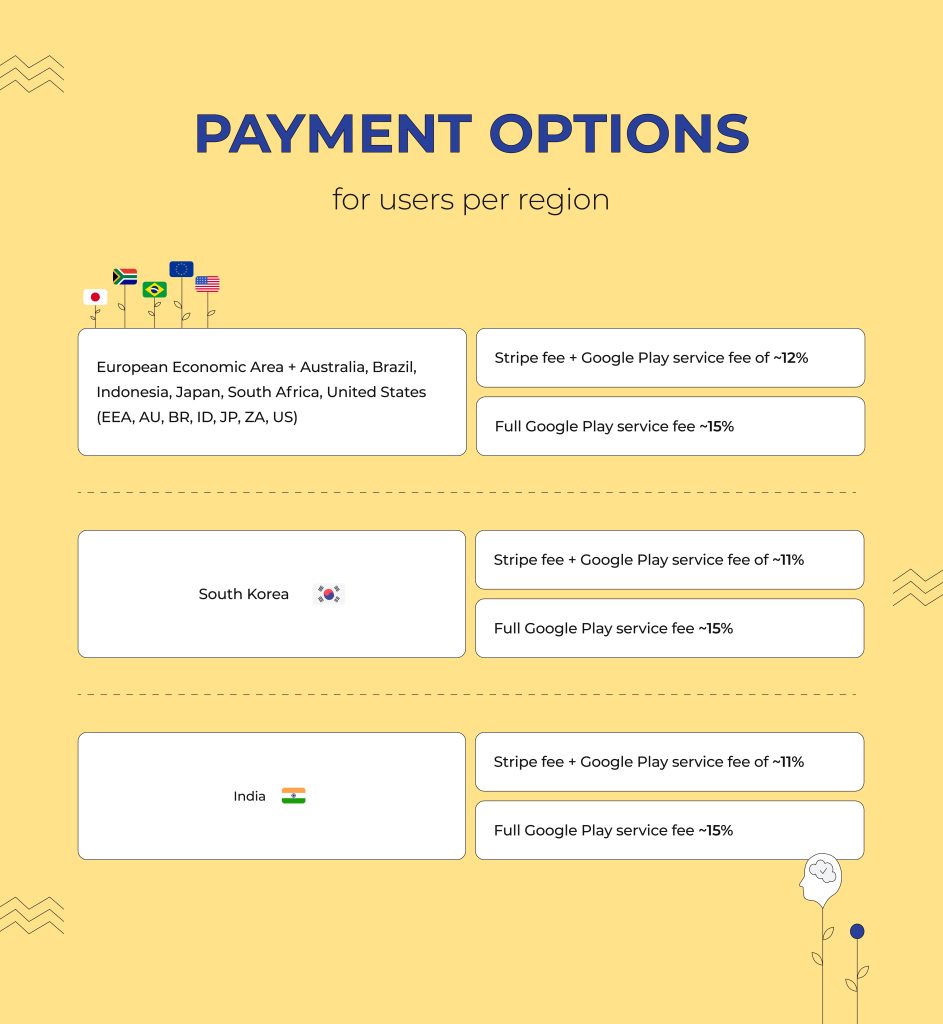

Apart from the launch of the above External Offers program, Google also unveiled additional code changes that the company says will facilitate alternative billing systems for in-app purchases. First, the tech giant allowed developers of non-gaming apps to offer their users in countries in the EEA an alternative to Google Play’s billing system when they are paying for digital content and services.

Whenever consumers opt for an alternative billing system, the service fee the developer pays will be reduced by 3%. So most developers will now pay a service fee of 12% or lower based on revenue made on transactions through alternative billing for accounts of EEA users acquired through the Play platform.

And just very recently, these have expanded to all developers whose apps reach EEA users.

Google Play’s billing system will continue to be required for apps and games distributed via Play to users in countries outside the EEA and for games distributed to users within the EEA.

How Apple complies with the DMA

More tech interoperability from Apple

Apple is now also allowing non-Apple payment processing tools, app stores and web browsers. Developers will have to assess whether those changes are positive for their bottom line on a case-by-case basis. You will find that fees differ slightly depending on the download volume and choice of payment processing tools.

After the March 2024 iOS 17.4 software update, Apple device users in the EU gained access to third-party tech. It is now possible for app owners to offer their users a link within the app to a web page collecting payments. This will require the ExternalPurchaseLink API to be implemented. Similarly to how it happens on Android, each time users click on such a link, they will receive a full-screen warning message. It will warn users that Apple is not responsible for the privacy or security of such purchases.

Fee structure for in-app purchases changes

Under the “Alternative Terms Addendum for Apps Distributed in the EU” scheme, Apple lowers its 30% commission on sales and in-app purchases. However, in certain cases, there will be some additional fees.

Merchants can now choose an external payment service provider (PSP) to have customers take payments through apps on Apple devices. Under the company’s new scheme, Apple’s commission on in-app transactions for digital goods and services is reduced to

17% or

10% for apps that make under $1 million per calendar year.

These rules only apply to payments in apps from the App Store.

To use Apple’s App Store payment processing, you’ll have to pay a 3% fee. Another option is to use an external PSP for a lower fee.

Apple device owners can now also use a different contactless payment app or third-party app marketplace as their default payment processor. Better yet, Apple now allows third-party mobile wallet apps to work for payments in brick-and-mortar stores outside the European Economic Area (EEA).

Remember This When Implementing Alternative Payments

Stick to your current payment system for just a bit longer

Adopting a more considerate, ‘wait and see’ approach before risking jumping the gun and taking a leap of faith is the best course of action for now. As there’s no hard deadline for acceptance, app developers are not under significant pressure to commit to the new payment terms. Why is it better not to jump ship just now? Well, switching to the new terms will result in irreversible changes to the entire developer account, thereby affecting all the apps created by one specific developer.

Think again about the Core Technology fee. If your app has many downloads, but its profitability per user is below 0.5 cents, you may end up paying more to Apple than you actually earn.

No significant pressure to revise your in-app payment just yet

Before you change your in-app payment strategies, look at the data and figures again. Sure, switching to accept an alternative payment collection method does look very appealing – you do get a reduced fee of 27% (3% lower). However, there’s a catch. Unfortunately, you can offer such an option in only place in your app.

What’s more, doing this will require additional action from users, who will have to take it before they’re even redirected to your company website. Moreover, once they get to the company website, they’ll have to log in once more, which will result in a less frictionless overall experience.

Choose the specific payment method wisely

Don’t forget to have each specific payment in the corresponding region. The region in question is not the one selected on your phone but the one set in your Google or Apple account, which you cannot easily change.

We’re currently preparing an additional neat guide for you with an overview of all the possible alternatives. In it, we will cover them in greater detail, so stay tuned.

More apps or more payment systems?

There are two ways to serve a specific region. One way is to have one app supporting alternative payment solutions depending on the region set in the account. Another one is to have two separate applications on the app store, each with a different region set in a Play Console developer account. Both ways have their pros and cons, which may depend on the application in question.

So, what is Applandeo’s advice at this point in time? Don’t rush and hold steady for now. The advantages are huge, but the risks are high as well. And we haven’t even touched upon the risk of fraudulent transactions.

Summary

The DMA is set to be a huge boon for app owners and developers alike. Thanks to it, they will no longer have to accept or sacrifice a 30% cut of all in-app purchases currently made in the Apple Store and Google Play Store, to say nothing of exorbitant commission fees—something akin to a digital ‘sales tax’. Sure, alternative app stores and payment systems will keep taking a huge cut, but they have fewer hidden fees and are much more flexible and open to negotiations, unlike such monoliths as Apple and Google are. And that’s just the tip of the iceberg and the very beginning of the liberalization process.

So, what exactly changed a month ago, on March 6, 2024? Well, not that much, really. All the changes we tried to cover above won’t fully affect app developers and end users for another 6 to 12 months. It will take at least a quarter more for all the different payment service providers, such as Stripe and PayPal, among others, in the entire ecosystem to realign anew. Making all the necessary technical changes while consulting the EU commission will take as much time, if not more.

The future growth being brought about by the DMA is exciting, but we’ll be advised to hold steady for just a bit more.

Are you looking for a tech partner? Searching for a new job? Or do you simply have any feedback that you'd like to share with our team?

Whatever brings you to us, we'll do our best to help you. Don't hesitate and drop us a message!

Explained - BANNER_Your-Go-To-Guide-To-DMA-360x161")